Our Correspondent

Kohima, Sep. 23 (EMN):

Our Correspondent

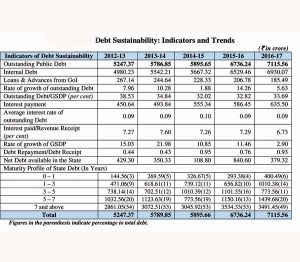

Kohima, Sep. 23 (EMN): The report of the Comptroller and Auditor General of India (CAG) on Nagaland’s finances for the year ending March 31 2017, which was presented in the Nagaland Legislative Assembly has underscored that timely submission of Utilisation Certificates (UCs) as a major area of worry for Nagaland.

According to the CAG, at the end of March 2017, 286 UC involving an aggregate financial amount of INR 909.61 cr. were pending for submission even after a lapse of one to six years from various departments. According to financial rules, UCs should be obtained by the departmental officers from the grantees for the grants provided for specific purposes; they should be forwarded to the Accountant General (Accounts & Entitlement) after verification, within 12 months from the date of their sanction unless specified otherwise.

There is an increase of 182 UC and funds amounting to INR 691.96 cr. in just a span of two years. The CAG highlighted that 104 UC involving an aggregate amount of Rs.217.65 cr. from different departments was pending for submission even after a lapse of 1-5 years.

The department of School Education tops the list in outstanding UC with a total 31 UC worth INR 142.19 cr. while the Health and Family Welfare department has 15 outstanding UC involving INR 90.9 cr.; Rural Development also has 15 pending UC for INR 90.8 cr.; Social Security and Welfare 20 UC for INR 54 cr.; Cooperation has five outstanding UC for INR 38.6 cr.; Youth Resources and Sports with 15 pending UC for INR 21.2 cr.; Fisheries with five UC for INR 3.15 cr.; and a total 190 UC from other departments involving INR 468.8 cr.

The report has pointed out that in the absence of UC it could not be ascertained if the recipients had used the grant for the purpose for which they were given. Noting that the departments had provided different sets of figures for outstanding UC thereby resulting in difference between the position of outstanding UC furnished by the departments and those given in the Finance Accounts, it highlighted the need to reconcile the difference.

Only 10% use from INR 38.78 cr. drawn by depts. (See table)

The CAG report has also revealed that INR 38.78 cr. was drawn by 14 departments during the year 2016-17 for implementation of schemes, out of which the departments had used only INR 4.19 cr. (10.8 percent) during said financial year. The remaining funds of INR 32.18 cr. was kept in civil deposit and INR 2.41 cr. in current bank accounts.

The departments are General Manager NST, Election, YRS, directorate of Science and Technology, Labour, Urban Development, Technical Education, Art and Culture, Evaluation, and IT &C, Commissioner of Taxes, Transport Commissioner, CE Irrigation and Flood Control, and director of Sericulture.

In addition to this, the report stated that information furnished by six banks (SBI, PNB, BoB, Vijaya Bank, HDFC and Axis Bank) revealed that an aggregate amount of INR 174.50 cr was lying in the respective bank accounts of 156 DDOs as on March 31, 2017. Out of this, an amount of INR 156.18 cr pertained to private banks with INR 155.52 cr in Axis Bank alone.

The CAG report stated that there were 25 cases of misappropriation, loss, defalcation etc. in 14 departments, private firms and others, involving government money to a tune of INR 230.33 cr up to the period 31 March 2017, on which final action was pending. The report noted that the highest amount of misappropriation and loss amounting to INR 74.83 cr involved in one case occurred in Youth Resources and Sports, where only an amount of INR 0.05 cr had been recovered so far.

The CAG report also revealed that 22 autonomous bodies/authorities have failed to submit 99 Annual Accounts due up to 2016-17 ranging between 1-7 years as of August 2017 to the Accountant General (Audit). They are the DRDAs of all the 11 districts, Nagaland State Legal Service Authority Kohima, Nagaland Board of School Education Kohima, State Institute of Rural Development Kohima, Development Authority of Nagaland Dimapur, Khadi and Village Industries Commission Dimapur, Nagaland Pollution Control Board Dimapur, NB&OCWWB Kohima, Nagaland State Agricultural Marketing Board Dimapur, NHK Kohima, Kohima Municipal Council and Mokokchung Municipal Council.

Due to the absence of Annual Accounts and subsequent audit of those 22 bodies and authorities, the CAG stated that proper accounting/utilisation of the grants and loans disbursed to them remained unverified in audit. Stating that reasons for non-preparation of the accounts were not intimated, the CAG report pointed out that non-submission and delay in annual accounts dilute the accountability of the authorities while defeating the very purpose of preparation of accounts.

On the delay in submission of Accounts/Audit Reports of autonomous bodies, the report said the annual account of the Nagaland Khadi and Village Industries Board (NKVIB) for the period 2015-17 had not been furnished as of August 2017 while the Nagaland Electricity Regulatory Commission (NERC) and Nagaland Hospital Authority were yet to furnish any account since their inception.

Meanwhile, 8 departmentally managed government commercial undertakings were yet to finalize their proforma accounts ranging from 1-37 years as on March 2017 even after a mention was made on the same in the CAG reports of 2012-13 and 2015. These undertakings are the Nagaland State Transport department, Nagaland Power Department, 3 farms under Agriculture, Changki Valley Fruit Preservation Factory, Timbre Treatment & Seasoning Plant Dimapur, Government Cottage Industries Emporia Kohima, 18 farms under Veterinary & Animal Husbandry, and Regional Progeny Orchard Lonnak under Horticulture department.

The report stated that absence of timely finalisation of accounts had made the government’s investment remain outside the scrutiny of the Audit/State Legislature, and corrective measures could not be taken in time. Such delay also opens the system to risk of fraud and leakage of public money, it added.

In its concluding remarks, the CAG has stated that non-submission of accounts in time indicates non-compliance with the financial rules. It maintained that audit reports can achieve desired results only if they evoked positive and adequate response from the administration.